》Check SMM silicon product quotes

》Order to view historical price trends of SMM metal spot cargo

SMM July 14th News:

As of July, the designed capacity for cold repair of PV glass has reached 3,600 mt/day, with actual production reduction exceeding 4,000 mt/day. Currently, the total cold repair capacity accounts for 29.47% of the total domestic PV glass capacity. Including blocked capacity, it is estimated that the current total operating capacity has fallen below 90,000 mt/day. The speed of production cuts on the supply side is moderate, and there are still plans for cold repair of some PV glass in the future. The confirmed designed capacity for cold repair in July remains at 1,400 mt/day, and 1,200 mt/day in August. Under the influence of the increasing scale of production cuts, some top-tier module enterprises have begun to plan to stock up in advance recently, and trading volume is expected to deviate from demand.

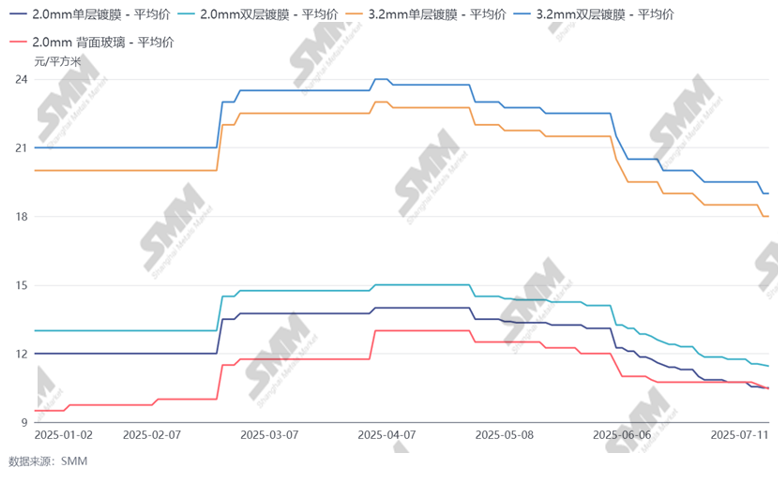

Figure: PV Glass Price Trends

Data Source: SMM

Since July, domestic glass prices have fallen again, with the industry's 2.0mm benchmark price approaching 10 yuan/m² and the negotiated price approaching 9.5 yuan/m². The loss pressure on glass enterprises continues to increase. Additionally, under the influence of the gradual decrease in module scheduled production, the glass inventory level is still rising slightly. Under this influence, the speed of glass production cuts has begun to accelerate. Although the current total operating capacity has approached about 70% of the total capacity, the expected production cuts planned according to the previous goals have not yet been achieved. Top-tier enterprises still have plans for further production cuts, but most of the subsequent plans will be determined based on the actual market situation.

However, due to the accelerated speed of glass production cuts and the expected increase in module scheduled production in September, the subsequent supply-demand balance will shift to supply being tight. Therefore, some top-tier module enterprises have begun to plan to stock up recently. It is expected that market trading volume will recover rapidly this week and next week, but there is an expected upper limit. Due to the lack of actual positive factors for modules in Q4, the stocking plans will also be more cautious. The procurement volume of each enterprise is expected to decrease compared with H1, mainly to meet their own in-plant inventory needs.

In terms of prices, it is expected that after this stocking, prices may rebound slightly from a low point in August, but mainstream transaction prices may not change significantly. Destocking takes priority, but currently, some upstream and downstream enterprises have differences in their expectations for subsequent prices. The main reason for the differences lies in the pressure of inventory levels. It is expected that prices will still be subject to negotiations in the near future.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)

![Silver Market Price Review and Expectations Brief Commentary (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/fNuSg20251217171735.jpg)